Calling this a "launch" requires some precision. What Tesla confirmed is the availability of FSD Supervised — a Level 2 advanced driver-assistance system that requires drivers to remain attentive and ready to intervene at all times. It is not unsupervised autonomy. CNBC reported that as recently as April 2026, Tesla's CFO confirmed the company was still awaiting full regulatory approval from Chinese authorities, and that the domestically available version is a localized variant — different from the more advanced V14 deployed in North America.

Still, the significance shouldn't be understated. Chinese consumers can access the feature for a one-time fee of 64,000 yuan (approximately $9,420) — a pricing structure Tesla discontinued globally in February 2026 when it shifted to a subscription model elsewhere.

The commercial stakes are substantial. FSD already has approximately 1.3 million subscribers in the United States, generating around $1.5 billion annually through its $99 monthly subscription fee. China is the world's largest new-energy vehicle market — and once FSD receives full approval, the potential software profit contribution from China could eventually exceed that of the U.S. market.

Reaching this point required building an entirely new data infrastructure inside China's borders. Tesla established a Shanghai data center in 2021 to ensure vehicle data remained stored domestically. In April 2024, the China Association of Automobile Manufacturers confirmed Tesla had satisfied four mandatory data security requirements, including anonymizing external facial data and processing in-vehicle data locally.

The most critical development came in February 2026. Tesla's Shanghai Lingang AI training center officially began operations, creating a full closed-loop system covering data collection, localized storage, domestic AI model training, vehicle deployment, and continuous iteration — allowing Chinese road-condition data to remain entirely within China throughout the AI training process.

Since 2020, Tesla has also collaborated with Baidu on map development, converting lane markings, traffic signals, and intersection topologies into formats compatible with FSD's visual system. Tesla has accumulated over 12 billion kilometers of global FSD driving data as of February 2026 — adding dense Chinese urban driving data would accelerate training on some of the world's most complex traffic environments.

This is what multi-year regulatory and technical groundwork looks like in practice. It isn't dramatic. It's unglamorous infrastructure work — and it's exactly what determines whether a technology actually deploys at scale.

Tesla's China FSD entry arrives into a market that hasn't been waiting patiently. According to CnEVPost, rivals including Xiaomi, Huawei, and XPeng have already integrated advanced urban intelligent driving systems as standard across their entire vehicle lineups — all trained on local Chinese road data. Chinese robotaxi firms Pony.ai and Baidu's Apollo Go are operating commercial, driverless ride-hailing services in Chinese cities today.

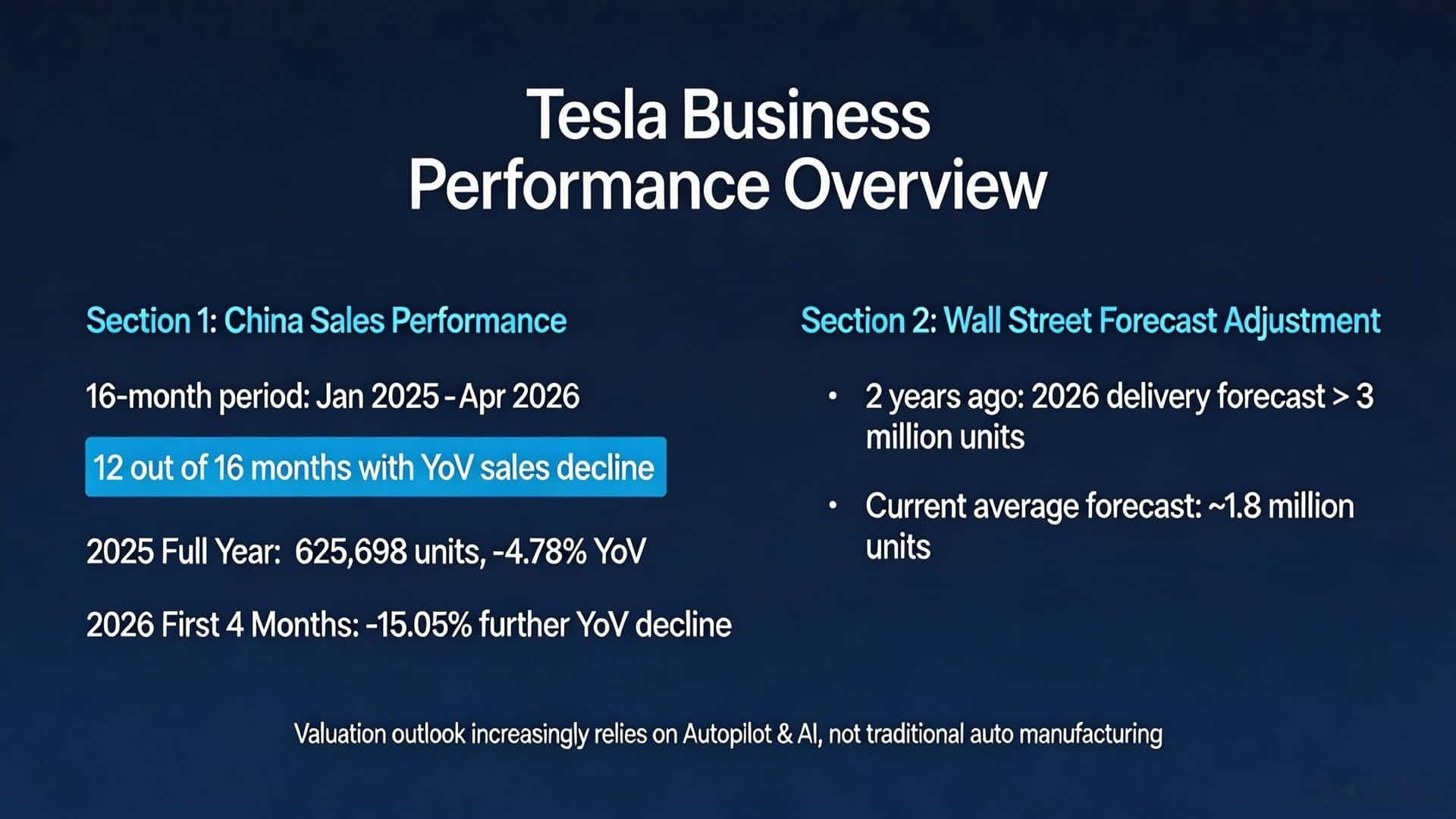

The sales numbers reflect this competitive gap. During the 16-month period from January 2025 to April 2026, Tesla saw year-on-year declines in monthly retail sales in China for 12 of those months. For the full year of 2025, retail deliveries totaled 625,698 units — down 4.78% year-on-year — and declined a further 15.05% in the first four months of 2026.

On the traditional auto business, Wall Street has cut expectations sharply. Two years ago, analysts projected Tesla would deliver more than 3 million vehicles in 2026; the average forecast now sits around 1.8 million. The case for a higher valuation increasingly hinges on autonomy and AI, rather than conventional carmaking.

FSD, in other words, isn't just a feature update. It's a strategic pivot.

The story of FSD in China is ultimately a story about how the EV industry matures. Early EV adoption was driven by hardware — battery range, charging speed, vehicle performance. The next competitive frontier is software: autonomous capability, over-the-air updates, AI-driven features that improve after purchase.

That shift has direct implications for the entire EV ecosystem. As software becomes the primary differentiator, the hardware layer — vehicles, charging infrastructure, grid connectivity — needs to be reliable enough to be invisible. Drivers won't think about whether their charging setup works. They'll expect it to, the same way they expect their phone to connect to Wi-Fi.

Tesla is also laying the groundwork to bring its latest Full Self-Driving (Supervised) software to China more broadly — recently updating its Chinese owner's manuals and website with references to features exclusive to FSD v14 and "Tesla Assisted Driving," which appears to be the local name it will use for FSD. The full-scale rollout is still pending comprehensive regulatory clearance, with Musk previously identifying Q3 2026 as a potential window.

Whether that timeline holds depends less on technology than on regulatory consensus. But the direction is clear: intelligent, software-defined vehicles are becoming the industry standard, not a premium option.

For EV owners building out their home or workplace charging setup ahead of that curve, mcevkeln.com covers the charging hardware fundamentals — a useful starting point as the broader EV ecosystem continues to evolve rapidly.

May 21st is a milestone, not a finish line. Full-scale FSD deployment across all eligible vehicles in China still requires comprehensive regulatory approval — and adapting to China's dense urban traffic, high concentration of electric scooters, and unique road infrastructure remains an ongoing technical challenge that no number of European precedents can shortcut.

The Dutch Vehicle Authority completed an 18-month safety assessment before approving FSD in the Netherlands in April 2026. South Korea, where FSD launched at the end of 2024, has already advanced to version V14.2. Each market is its own compliance project.

What Tesla has demonstrated is that the path exists — and that the work required to walk it is mostly unglamorous, methodical, and institutional. That's true for autonomous driving software. It's true for charging infrastructure at scale. It's true for every layer of the EV ecosystem that needs to become ordinary before electrification can become universal.

The extraordinary is still becoming the everyday. That process is simply further along than it was a year ago.